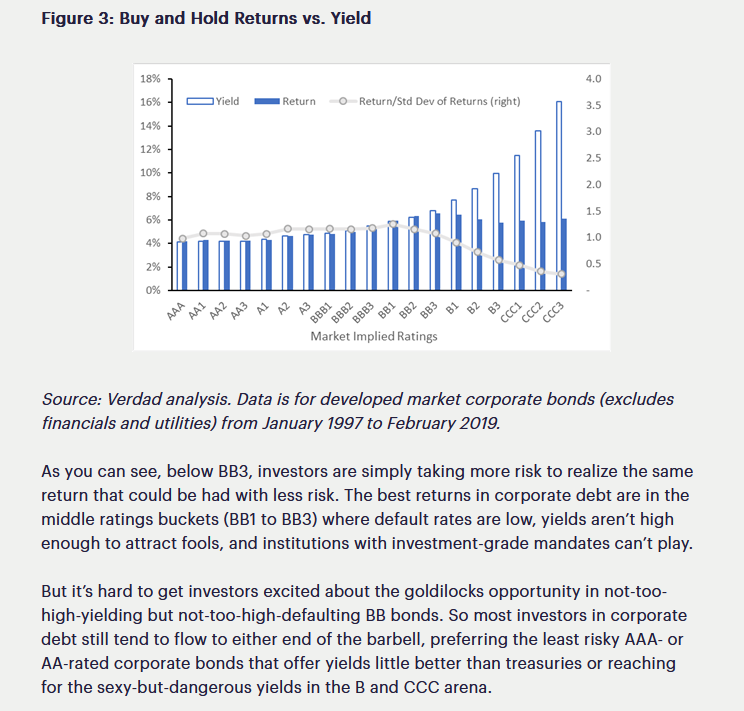

The best returns in corporate credit are those with the BB1 to BB3 credit ratings

The difference is most stark in BB and B rated bonds – and it is here we see a growing problem for credit investors. We call this problem “fool’s yield.” This is the yield above which the losses from defaults overcome the higher coupon payments and investors end up earning lower total returns than they would have buying lower yielding, higher rated bonds. Like fool’s gold, fool’s yield is shiny and attractive on the surface but worthless to the trained eye.

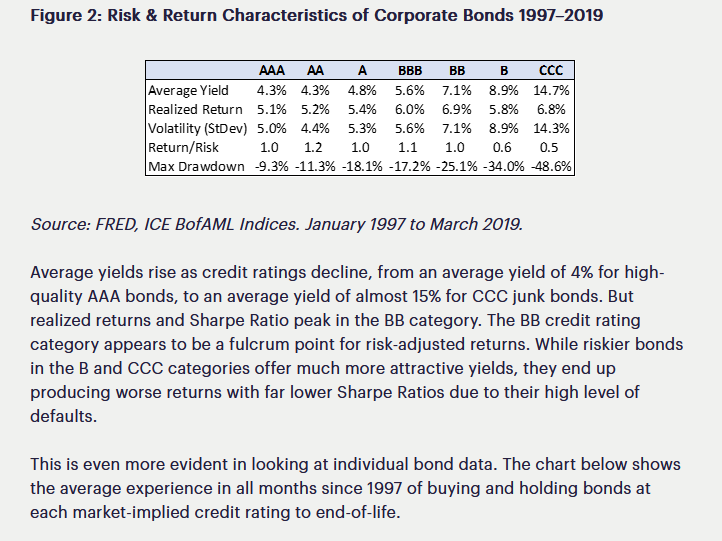

A study of long-term credit market data reveals that fool’s yield is a persistent phenomenon in corporate credit markets. Over the past 22 years, bonds rated B and CCC have had lower total returns and a much lower Sharpe Ratio (return/risk ratio) than higher rated, but lower yielding, BB bonds.